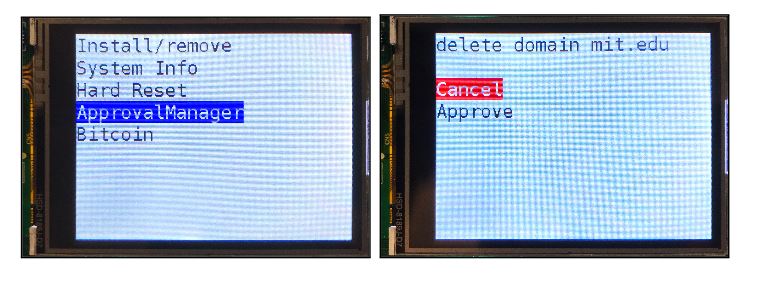

Researchers at the Massachusetts Institute of Technology’s Computer Science and Artificial Intelligence Laboratory (MIT CSAIL) have been working on a new secure cryptocurrency hardware wallet, dubbed Notary.

According to the recently published technical paper, the new secure hardware wallet will run as a USB stick with a small display and buttons. Notary wallet has a set of hardware fail-safes designed to mitigate successful cyber attacks. Known as “reset-based switching,” the wallet will reset the CPU, memory, and other hardware components when a user switches between one app to another.

MIT researchers claim that Notary is way secure than any other existing commercial cryptocurrency hardware wallets as Notary eliminates entire classes of bugs that affect existing wallets and also may be able to enhance the overall security of transaction approval.

Notary follows the same approach as existing hardware wallets for handling device loss. The user backs up their master key so it can be restored to a new device. To prevent an adversary from using the lost device, Notary requires the user to enter a PIN to access any functions, with retry limits and hard reset after sufficiently many failures.